PinnedPropTech@ecyYA Major Challenge in Machine Learning Applications: InterpretabilityMisconceptions Surrounding Rule GenerationNov 9, 2023Nov 9, 2023

PinnedPropTech@ecyYinDialogue & DiscourseUse DW Model To Master Housing Market DynamicsWhat are the causes of the global real house prices upheaval? It may sound complicated to understand all the market dynamics in one…Feb 26, 2023Feb 26, 2023

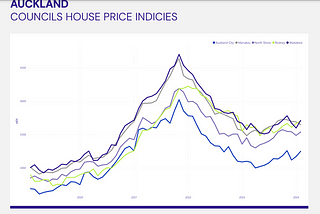

PropTech@ecyYRoller Coaster like Auckland House PricesThe Auckland housing market experienced significant fluctuations during the pandemic period. Before the pandemic, it fluctuated around…Apr 3Apr 3

PropTech@ecyYA Python Code of Geofencing Statistical Areas for Retail Catchment AnalysisWhat is geofencing?Jan 26Jan 26

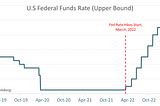

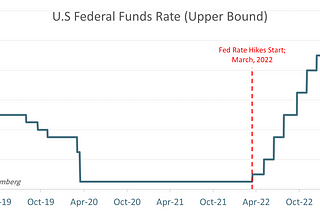

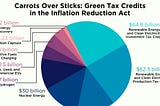

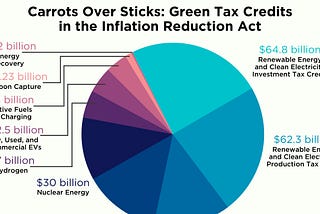

PropTech@ecyYinDialogue & DiscourseWill Inflation Rebound? A Review of the Patterns of 100 Inflation Events Since the 1970sIn response to the remarkable surge in US interest rates since 2022, projected to reach its peak in 2024, inflation rates in Europe and the…Jan 13Jan 13

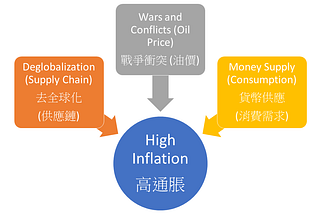

PropTech@ecyYinDialogue & DiscourseAnticipating an Oil Price Battle in 2024: The Dynamics of Oil Price Control and its Impact on…This article examines the trends of inflation in 2024, focusing on the three primary causes: the reduction in the U.S. M2 money supply, the…Jan 7Jan 7

PropTech@ecyYinDialogue & Discourse2024 Economic Vision: Decoupling Realities through Re-Industrialization and Self-SufficiencyIn a remarkable validation of predictions made in my articles (Yiu, 2020a, 2020b) from April 2020, the dawn of 2024 unveils an economic…Dec 31, 2023Dec 31, 2023

PropTech@ecyYinDialogue & DiscourseNew Zealand Courts’ Guidelines on Generative AI in Legal ProceedingsIn substantiating my prediction outlined in the article titled “A New Job Created by ChatGPT” on June 1, 2023, the New Zealand courts have…Dec 23, 2023Dec 23, 2023

PropTech@ecyY[Building Surveying Case Study] Unraveling the Leaky Homes Conundrum: Navigating Responsibility…New Zealand’s predicament with leaky homes has been characterized as the nation’s most extensive and costly man-made crisis. Approximately…Dec 4, 2023Dec 4, 2023

PropTech@ecyY[Building Surveying Case Study] Court Orders Demolition of Unauthorized Six-Storey Building in UKIn a recent court case that unfolded in the Birmingham High Court, the judge has issued a groundbreaking order mandating the demolition of…Nov 26, 2023Nov 26, 2023

![[Building Surveying Case Study] Court Orders Demolition of Unauthorized Six-Storey Building in UK](https://miro.medium.com/v2/resize:fill:160:106/1*RiLMqemL0ot0V9rU5wCr1w.png)

![[Building Surveying Case Study] Court Orders Demolition of Unauthorized Six-Storey Building in UK](https://miro.medium.com/v2/resize:fill:320:214/1*RiLMqemL0ot0V9rU5wCr1w.png)